Top 5 Diamond-Producing Countries in Africa (2024–2026 Insight): Real Output, Money Flow, and How the Industry Actually Works

In the business world, one thing that quietly decides who survives and who shuts down is steady funding. A lot of businesses don’t fail because the idea is bad, but because the cash flow is weak or inconsistent. That is why many operators, especially in Africa, lean heavily on structured financing systems like microfinance banks and loan facilities to keep things running while waiting for profit to stabilize.

Now, when you zoom into industries like mining—especially diamonds—you start to see how money, government policy, and global demand all connect. Africa remains one of the strongest regions in the world for natural diamond production, not just in volume but in value. Even though global pressure from lab-grown diamonds and market shifts has slowed things down a bit between 2024 and 2026, African countries are still central players in the supply chain.

Top Diamond-Producing Countries in Africa

Africa is not just part of the diamond market, it is the backbone of it in terms of quality and global value. Here are the key countries consistently leading production:

1. Botswana

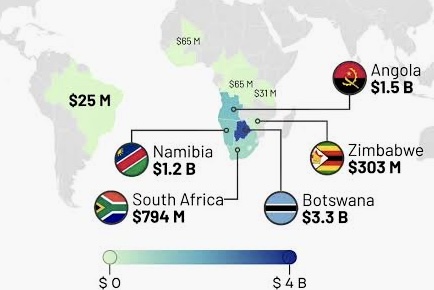

Botswana is still the strongest diamond country in Africa, and in many cases, the world when you look at value instead of just volume. The country produces roughly 25–28 million carats depending on the year, and its stones are highly valued due to quality. Mines like Jwaneng and Orapa are among the richest globally. Diamonds also contribute massively to Botswana’s economy, forming a large part of export revenue and GDP. However, in recent times, production has been slightly reduced due to global demand slowdown and stockpile pressure.

2. Angola

Angola has been growing aggressively in the diamond sector. Recent figures place its output around 10–17 million carats depending on mining activity and reporting period. What makes Angola important is not just volume but increasing quality and improved government structure in the sector. Companies like Endiama and major mines such as Catoca and Luele are pushing Angola closer to the top tier globally.

3. Democratic Republic of Congo (DRC)

The DRC produces a large amount of diamonds, but most of it comes from artisanal and small-scale mining. Output is high, but value per carat is much lower compared to Botswana or Angola due to quality differences. The country still plays a major role in global supply, but faces challenges like regulation, tracking, and formalization of mining operations.

4. South Africa

South Africa is where modern diamond mining in Africa started, and it still holds strong historical and industrial importance. Production is lower compared to peak years, but the quality remains high. Mines like Venetia (owned by De Beers) still produce valuable stones. The country is also more focused on beneficiation—cutting, polishing, and adding value locally rather than exporting raw stones.

5. Namibia and Zimbabwe (close competition)

Namibia is known for offshore diamond mining, which produces fewer but very high-value stones. Zimbabwe also maintains solid production levels through both formal and informal mining channels. In some reports, Lesotho appears strongly in terms of extremely high-value rare diamonds, even though volume is smaller.

How the Diamond Industry Actually Works (Simple Breakdown)

The diamond business is not just digging and selling stones. It is a full chain that includes exploration, mining, sorting, valuation, cutting, polishing, and final retail.

Most African countries are now trying to move away from exporting raw diamonds only. The focus is shifting toward beneficiation—meaning keeping more value inside the country by processing stones locally. This is where more jobs and long-term income are created.

Companies like De Beers and government-linked firms still control large portions of the supply chain, especially in Botswana through joint ventures like Debswana.

Starting or Entering the Diamond Business (Real Talk Guide)

Getting into diamonds is not something casual. It requires capital, knowledge, and strong trust networks.

First, understanding the value system is important. Diamonds are priced based on the 4Cs: carat, cut, clarity, and color. Without this knowledge, it is very easy to lose money.

Most successful people in this space did not start by buying and selling immediately. They started by working around the industry—jewelry shops, mining companies, or trading firms—learning how grading and pricing actually works.

Networking is also very important. Trade shows and mining conferences are where deals are built. In Africa, countries like Botswana, South Africa, and Angola regularly host or participate in global mining events.

Legally, you cannot just enter mining or trading without proper licensing. Many countries now enforce strict rules under the Kimberley Process to avoid conflict diamonds.

Money Reality, Risks, and Business Flow

Diamond business is high risk and high reward, but it is not stable income like salary jobs.

A small trader might start with millions of naira equivalent just to access small polished stones. Larger operations deal in millions of dollars per transaction. But losses are also common due to pricing mistakes, fake stones, or market drops.

For African economies, diamonds still bring in billions in export revenue, but dependence is slowly reducing as countries diversify into other minerals and industries.

Industry Shifts (2025–2026 Trends)

One major shift is the rise of lab-grown diamonds. These are cheaper and widely available, which is affecting natural diamond prices globally.

Another shift is production control. Countries like Botswana have reduced output in response to global market pressure, while Angola is increasing production and expanding international partnerships.

There is also a strong push toward traceability—tracking where every diamond comes from to prove ethical sourcing.

Challenges and Controversies

The diamond industry is not without problems.

Artisanal mining in parts of the DRC and other regions still faces issues like poor regulation and environmental concerns. The Kimberley Process was created to reduce conflict diamonds, but enforcement is still not perfect everywhere.

There is also ongoing debate about whether local communities benefit enough from the wealth generated by mining companies.